Financing Facing Possessions: How will you avail Taxation benefits from LAP?

17 януари, 2025

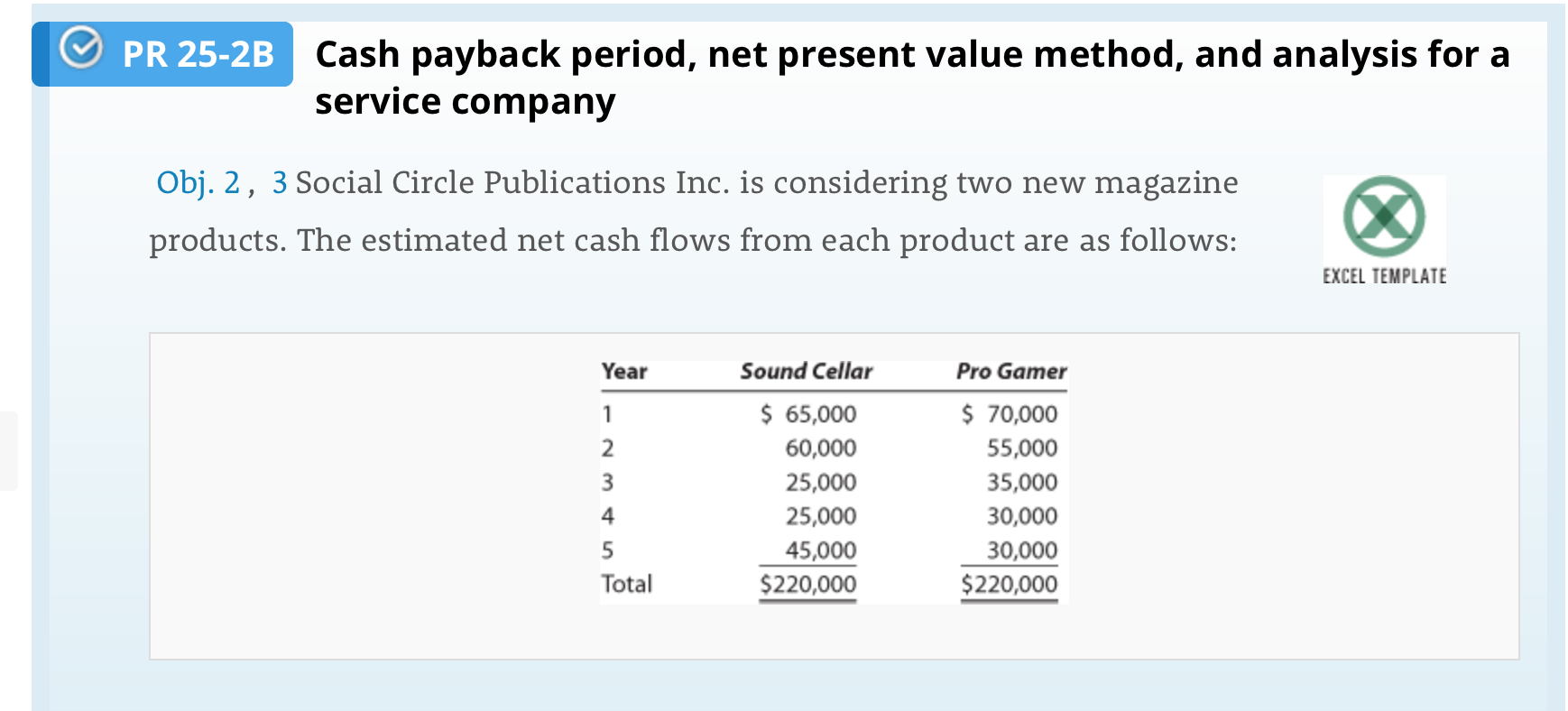

It’s something https://paydayloanalabama.com/smoke-rise/ which we have all explored will eventually in our lives when we now have confronted a significant financial difficulties. As opposed to attempting to sell the house outright and shedding ownership, placing it upwards since safety having a loan company is obviously an exceptional alternative.

When contrasting the choices, understand that just the notice paid is approved to possess a benefit, perhaps not the primary costs. Point 37 (1) to possess industrial objectives, or area 24 (b) to own investment almost every other assets, can be used to allege attract costs to possess home mortgage taxation positives.

It is possible to qualify for income tax coupons if you take out financing Up against Assets. Below are a few examples:

Taxation benefit below 24(B)

This point lets salaried people to gain benefit from the Loan Facing Property tax work for. You are entitled to income tax write-offs to Rs dos lakh if you use the borrowed funds Up against Property total loans their brand new residential household. The attention payments qualify to have tax write-offs.

Taxation Work with lower than Point 37 (1):

It clause of your Tax Act exclusively applies to costs, not money, as many individuals believe. Because of this, if you have one costs connected with your online business functions that commonly money or private costs, contain them on your money/loss statement.

A loan facing property is maybe not income tax-deductible, it doesn’t matter if the borrowed funds was created getting providers otherwise personal reasons. When you are investing in assets in return for currency when you take aside a home loan, the mortgage age holds true (somewhat) when it comes to organization agencies purchasing industrial property. Financing against assets, likewise, shows that your debt currency of the pledging your home, and so this contribution is not income tax-allowable.

No Income tax Exemptions Enjoy from the Following Conditions:

There are numerous areas within the Point 80C that enable you to claim tax advantages. Even although you provides an active household loan, you can qualify for tax positives; not, there aren’t any tax positives getting Financing Facing Possessions significantly less than Area 80C of your own Interior Funds Password.

House Very first Monetary institution Loan Up against House is best for consumers who are in need of fund rapidly, whether they very own residential or industrial assets. The financial institution gives you the following gurus:

- Your business needs, you can purchase a loan to 50% of property’s value.

- Special offers are around for physicians, who will use to 70% of your property’s really worth.

- To have non-organization consumers, there are not any prepayment charges.

- Glamorous interest levels to the transfers of balance are available.

- Have fun with a loan Facing Possessions to fulfill your otherwise company needs.

- 20-seasons EMIs at an affordable price

- Score a loan all the way to Rs fifty Lakh.

- Vehicles Pre-shell out and you can region-fee options are including readily available.

Tax Masters above-upwards Loans:

Present home loan individuals can apply for a type of financing known as an effective top-right up financing, which includes lower interest levels than unsecured loans. The major-right up mortgage can be utilized for any mission provided they employs the new financing economic institution’s laws and regulations.

Top-upwards financing taxation experts will be stated when you yourself have all of the of one’s required invoices and documents to prove your better-up loan was applied towards the acquisition, construction, resolve, or renovation away from a house.

Compared with the brand new Rs. dos lakh deductions offered on the interest money; the highest deduction permitted is actually Rs. 29,000. That it deduction is just offered in the event your property is self-occupied. There isn’t any maximum with the deduction which is often advertised if your possessions try hired away in the course of the brand new fixes and you may home improvements.

However, the maximum lay-out of which is often stated up against other resources of money when you look at the any monetary year has been Rs. 2 lakhs. If your interest changed, if one earns more than Rs. 2 lakhs during the a certain monetary season, they can take it send for approximately 8 years.

Though of the market leading-up fund, the latest income tax professionals with the financing up against possessions are principally influenced by the main repayment regarding the utilization of the fund. Whether your financing were utilized to cultivate otherwise buy an alternative property, brand new taxation deduction might be reported lower than areas 80C and you will 24 (b), correspondingly. not, whether your funds were utilized for assets repairs, renovations, otherwise changes, zero deduction for the principal fees will be claimed.